3 hours ago

Itron Inc. (NASDAQ:ITRI) is one of the 10 technology stocks offering more than 50% upside.

On May 26, Itron Inc. (NASDAQ:ITRI) announced the expansion of its strategic collaboration with Hunter Water. The purpose of this partnership is to help accelerate the utility’s digital water transformation through its formalized Digital Metering Pilot Program. It uses advanced data tracking to reduce non-revenue water loss and radically improve water network management.

Copyright: kosmos111 / 123RF Stock Photo

At the same time, the program makes it possible for consumer-side consumption transparency to boost long-term conservation initiatives. Itron Intelis wSource NB-IoT ultrasonic water meters are specifically integrated as part of the utility’s deployment of a diversified ****** et mix as a core operational phase. Additionally, these deployed devices will be managed through Temetra, Itron’s cloud-based, multi-vendor, multi-commodity meter data management solution, which is already in use by the utility.

Apart from these recent developments, ****** yst ratings also indicate promising prospects for the stock. Back on April 29, Roth Capital ****** yst Chip Moore updated his view of Itron Inc. (NASDAQ:ITRI) after the company reported its first quarter earnings and shared a lower second quarter forecast relative to market consensus. Moore maintained his Buy rating on the shares. He decreased the firm’s price target from $150 to $136, which still results in an upside potential of almost 65%.

On May 26, Itron Inc. (NASDAQ:ITRI) announced the expansion of its strategic collaboration with Hunter Water. The purpose of this partnership is to help accelerate the utility’s digital water transformation through its formalized Digital Metering Pilot Program. It uses advanced data tracking to reduce non-revenue water loss and radically improve water network management.

Copyright: kosmos111 / 123RF Stock Photo

At the same time, the program makes it possible for consumer-side consumption transparency to boost long-term conservation initiatives. Itron Intelis wSource NB-IoT ultrasonic water meters are specifically integrated as part of the utility’s deployment of a diversified ****** et mix as a core operational phase. Additionally, these deployed devices will be managed through Temetra, Itron’s cloud-based, multi-vendor, multi-commodity meter data management solution, which is already in use by the utility.

Apart from these recent developments, ****** yst ratings also indicate promising prospects for the stock. Back on April 29, Roth Capital ****** yst Chip Moore updated his view of Itron Inc. (NASDAQ:ITRI) after the company reported its first quarter earnings and shared a lower second quarter forecast relative to market consensus. Moore maintained his Buy rating on the shares. He decreased the firm’s price target from $150 to $136, which still results in an upside potential of almost 65%.

10 hours ago

By Adriana Barrera

MEXICO CITY, June 2 (Reuters) - Mexico's sugar industry is pushing for the United States to eliminate limits on U.S. imports and is working on a potential anti-dumping case against U.S. fructose should talks on the issue fail, industry representatives said on Tuesday.

Mexico produces cane sugar across half its states and its producers, mill operators and day laborers are politically influential.

National Agricultural Council (CNA) representative Juan Cortina told reporters the U.S. had in recent years applied a measure called "future imports subject to tariffs" that drastically reduced the quota of sugar imports allowed from Mexico.

Sugar was subject to the North American Free Trade Agreement until 2014, when the U.S. became Mexico's main sugar market, but dumping accusations in the U.S. led to strict import caps and minimum prices.

MEXICO CITY, June 2 (Reuters) - Mexico's sugar industry is pushing for the United States to eliminate limits on U.S. imports and is working on a potential anti-dumping case against U.S. fructose should talks on the issue fail, industry representatives said on Tuesday.

Mexico produces cane sugar across half its states and its producers, mill operators and day laborers are politically influential.

National Agricultural Council (CNA) representative Juan Cortina told reporters the U.S. had in recent years applied a measure called "future imports subject to tariffs" that drastically reduced the quota of sugar imports allowed from Mexico.

Sugar was subject to the North American Free Trade Agreement until 2014, when the U.S. became Mexico's main sugar market, but dumping accusations in the U.S. led to strict import caps and minimum prices.

18 hours ago

We recently compiled a list of the 11 Most Undervalued Pharma Stocks to Invest In. Gilead Sciences, Inc. (NASDAQ:GILD) is one of the most undervalued stocks to invest in.

TheFly reported on May 27 that GILD presented long-term interim findings from the ongoing Phase 3 ***** URE study of Livdelzi at the 2026 European ***** ociation for the Study of the Liver Congress in Barcelona. A post hoc ***** ysis showed sustained improvement in liver function markers among patients with primary biliary cholangitis who had persistently elevated alkaline phosphatase despite prior first-line therapy.

Across treated participants, ALP levels declined, and a high proportion achieved biochemical normalization over extended follow-up, with durable responses observed up to two years. Additional ***** yses indicated stability in other indicators of cholestasis and liver stiffness over time. The safety profile remained consistent with earlier findings, with no treatment discontinuations due to adverse events and no new safety concerns identified.

In an interconnected pipeline development, Gilead Sciences, Inc. (NASDAQ:GILD) announced on May 22 that the European Medicines Agency’s CHMP issued a positive opinion recommending marketing authorization for Trodelvy (sacituzumab govitecan-hziy) as a first-line monotherapy option for adult patients with unresectable locally advanced or metastatic triple-negative breast cancer who are not eligible for PD-1 or PD-L1 inhibitor therapy.

The decision is based on Phase 3 ASCENT-03 results demonstrating statistically significant and clinically meaningful improvement in progression-free survival compared with standard chemotherapy, including a 38% reduction in the risk of disease progression or death. Metastatic TNBC remains a highly aggressive cancer with limited first-line options and poor outcomes. The recommendation now proceeds to the European Commission for final review, with a decision expected later in 2026.

TheFly reported on May 27 that GILD presented long-term interim findings from the ongoing Phase 3 ***** URE study of Livdelzi at the 2026 European ***** ociation for the Study of the Liver Congress in Barcelona. A post hoc ***** ysis showed sustained improvement in liver function markers among patients with primary biliary cholangitis who had persistently elevated alkaline phosphatase despite prior first-line therapy.

Across treated participants, ALP levels declined, and a high proportion achieved biochemical normalization over extended follow-up, with durable responses observed up to two years. Additional ***** yses indicated stability in other indicators of cholestasis and liver stiffness over time. The safety profile remained consistent with earlier findings, with no treatment discontinuations due to adverse events and no new safety concerns identified.

In an interconnected pipeline development, Gilead Sciences, Inc. (NASDAQ:GILD) announced on May 22 that the European Medicines Agency’s CHMP issued a positive opinion recommending marketing authorization for Trodelvy (sacituzumab govitecan-hziy) as a first-line monotherapy option for adult patients with unresectable locally advanced or metastatic triple-negative breast cancer who are not eligible for PD-1 or PD-L1 inhibitor therapy.

The decision is based on Phase 3 ASCENT-03 results demonstrating statistically significant and clinically meaningful improvement in progression-free survival compared with standard chemotherapy, including a 38% reduction in the risk of disease progression or death. Metastatic TNBC remains a highly aggressive cancer with limited first-line options and poor outcomes. The recommendation now proceeds to the European Commission for final review, with a decision expected later in 2026.

22 hours ago

Schafer Cullen Capital Management, Inc., an independent investment advisor, released its Q1 2026 investor letter for the “Small Cap Value Equity Strategy.” You can download a copy of the letter here. U.S. equity markets started 2026 with notable volatility due to geopolitical events and shifting macro conditions. The Russell 2000 rose 0.9% for the quarter, with small-cap value outperforming growth. Concerns over AI and its impact on software companies heightened among investors. The Small Cap Value Equity strategy composite returned -1.8% (gross) and -2.0% (net) in the quarter, while the Russell 2000 Value returned 5.0% for the quarter, and the broader Russell 2000 Index gained 0.9%, reflecting strength in small caps. The performance in the quarter was shaped by rising interest rates, widening credit spreads, and geopolitical tensions. Overall, the quarter challenged quality-oriented strategies, yet the firm remains committed to investing in companies with strong balance sheets and sustainable earnings, believing this focus will benefit as market conditions improve. In addition, please check the Strategy’s top five holdings to know its best picks in 2026.

In its first-quarter 2026 investor letter, Schafer Cullen Capital Small Cap Value Equity Strategy highlighted stocks like Crocs, Inc. (NASDAQ:CROX). Crocs, Inc. (NASDAQ:CROX) is a leading casual lifestyle footwear and accessories company best known for its iconic clogs. On June 1, 2026, Crocs, Inc. (NASDAQ:CROX) closed at $119.28 per share. One-month return of Crocs, Inc. (NASDAQ:CROX) was 15.87%, and its shares gained 16.75% over the past 52 weeks. Crocs, Inc. (NASDAQ:CROX) has a market capitalization of $5.93 billion.

Schafer Cullen Capital Small Cap Value Equity Strategy stated the following regarding Crocs, Inc. (NASDAQ:CROX) in its Q1 2026 investor letter:

"Performance was driven by Under Armour (45.2%), Marriott Vacations (14.2%), and Crocs, Inc. (NASDAQ:CROX) (13.3%), reflecting strength in branded apparel and leisure demand. Sales: Crocs Inc. (CROX): While the company continues to execute well operationally, the valuation became less compelling relative to other opportunities within the portfolio and its HeyDude brand continues to experience growth issues."

Crocs, Inc. (NASDAQ:CROX) is not on our list of 40 Most Popular Stocks Among Hedge Funds Heading Into 2026. According to our database, 44 hedge fund portfolios held Crocs, Inc. (NASDAQ:CROX) at the end of the first quarter, compared to 40 in the previous quarter. in Q1 2026, Crocs, Inc. (NASDAQ:CROX) generated enterprise revenue of $921 million, down 2% to prior year on a reported basis. While we acknowledge the potential of Crocs, Inc. (NASDAQ:CROX) as an investment, we believe certain AI stocks offer greater upside potential and carry less downside risk. If you're looking for an extremely undervalued AI stock that also stands to benefit significantly from Trump-era tariffs and the onshoring trend, see our free report on the best

In its first-quarter 2026 investor letter, Schafer Cullen Capital Small Cap Value Equity Strategy highlighted stocks like Crocs, Inc. (NASDAQ:CROX). Crocs, Inc. (NASDAQ:CROX) is a leading casual lifestyle footwear and accessories company best known for its iconic clogs. On June 1, 2026, Crocs, Inc. (NASDAQ:CROX) closed at $119.28 per share. One-month return of Crocs, Inc. (NASDAQ:CROX) was 15.87%, and its shares gained 16.75% over the past 52 weeks. Crocs, Inc. (NASDAQ:CROX) has a market capitalization of $5.93 billion.

Schafer Cullen Capital Small Cap Value Equity Strategy stated the following regarding Crocs, Inc. (NASDAQ:CROX) in its Q1 2026 investor letter:

"Performance was driven by Under Armour (45.2%), Marriott Vacations (14.2%), and Crocs, Inc. (NASDAQ:CROX) (13.3%), reflecting strength in branded apparel and leisure demand. Sales: Crocs Inc. (CROX): While the company continues to execute well operationally, the valuation became less compelling relative to other opportunities within the portfolio and its HeyDude brand continues to experience growth issues."

Crocs, Inc. (NASDAQ:CROX) is not on our list of 40 Most Popular Stocks Among Hedge Funds Heading Into 2026. According to our database, 44 hedge fund portfolios held Crocs, Inc. (NASDAQ:CROX) at the end of the first quarter, compared to 40 in the previous quarter. in Q1 2026, Crocs, Inc. (NASDAQ:CROX) generated enterprise revenue of $921 million, down 2% to prior year on a reported basis. While we acknowledge the potential of Crocs, Inc. (NASDAQ:CROX) as an investment, we believe certain AI stocks offer greater upside potential and carry less downside risk. If you're looking for an extremely undervalued AI stock that also stands to benefit significantly from Trump-era tariffs and the onshoring trend, see our free report on the best

1 day ago

Access to this page has been denied because we believe you are using automation tools to browse the website.

This may happen as a result of the following:

Please make sure that Javascript and cookies are enabled on your browser and that you are not blocking them from loading.

Reference ID: #0d4e1770 -5f75-11f1-becf-6db24b82b72a

This may happen as a result of the following:

Please make sure that Javascript and cookies are enabled on your browser and that you are not blocking them from loading.

Reference ID: #0d4e1770 -5f75-11f1-becf-6db24b82b72a

1 day ago

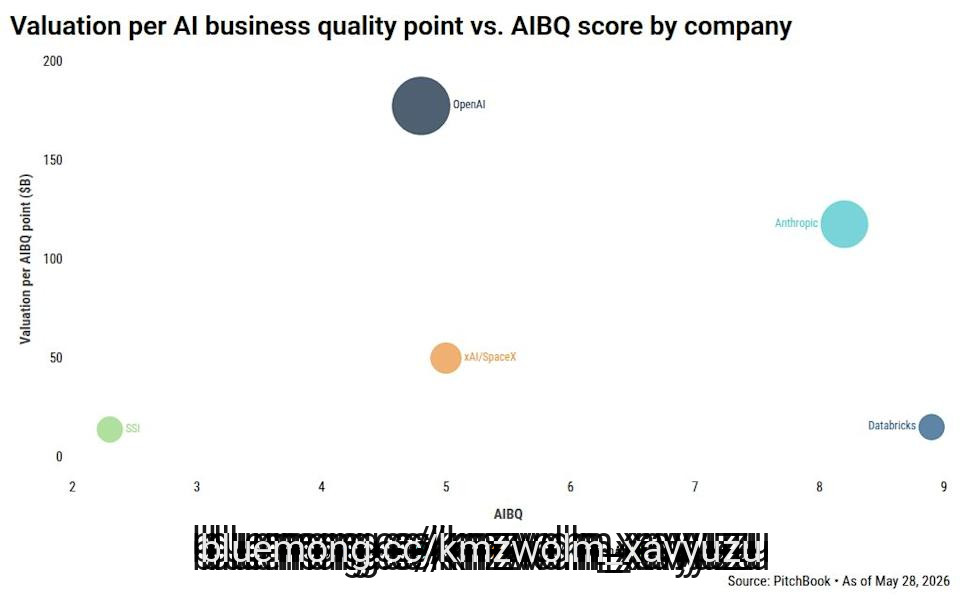

OpenAI is going public as the most expensive AI company in its peer group—not by market cap, but by what investors are paying for each unit of business quality, according to our latest research. The company’s upcoming disclosures will test whether that premium is justified or just momentum.

OpenAI’s path to profitability rests on a contract with an expiration date. In April, it renegotiated its revenue-share agreement with Microsoft, capping payments at $38 billion through 2030 and saving an estimated $70 to $97 billion. Without that cap, positive free cash flow is not possible. Investors must price the listing based on an agreement whose most consequential provisions haven’t been written.

The company’s revenue is real, but the economics are broken. Q1 revenue hit $5.7 billion, yet at a negative 122% adjusted operating margin, OpenAI spent $2.22 for every dollar earned. To justify an $852 billion valuation, the company would need to generate $95 billion to $105 billion in free cash flow by 2030. Based on Q1 numbers, it is on track to lose between $10 billion and $30 billion that year instead.

Sign up for The Daily Pitch newsletter Subscribe

Our AI Business Quality (AIBQ) scorecard puts OpenAI last among its peers at 4.8 out of 10. At an $852 billion valuation, that works out to $177.5 billion per AIBQ point—11.8 times what investors pay for Databricks. Its main competitor, Anthropic, is pursuing a parallel listing with higher run-rate ARR (estimated $47 billion vs. $25 to $33 billion for OpenAI), a faster path to profitability, and the enterprise market share lead (40% vs. 27%).

OpenAI’s path to profitability rests on a contract with an expiration date. In April, it renegotiated its revenue-share agreement with Microsoft, capping payments at $38 billion through 2030 and saving an estimated $70 to $97 billion. Without that cap, positive free cash flow is not possible. Investors must price the listing based on an agreement whose most consequential provisions haven’t been written.

The company’s revenue is real, but the economics are broken. Q1 revenue hit $5.7 billion, yet at a negative 122% adjusted operating margin, OpenAI spent $2.22 for every dollar earned. To justify an $852 billion valuation, the company would need to generate $95 billion to $105 billion in free cash flow by 2030. Based on Q1 numbers, it is on track to lose between $10 billion and $30 billion that year instead.

Sign up for The Daily Pitch newsletter Subscribe

Our AI Business Quality (AIBQ) scorecard puts OpenAI last among its peers at 4.8 out of 10. At an $852 billion valuation, that works out to $177.5 billion per AIBQ point—11.8 times what investors pay for Databricks. Its main competitor, Anthropic, is pursuing a parallel listing with higher run-rate ARR (estimated $47 billion vs. $25 to $33 billion for OpenAI), a faster path to profitability, and the enterprise market share lead (40% vs. 27%).

2 days ago

House of Doge is pushing Dogecoin further into regulated fintech infrastructure through a new partnership with Paxos, giving the meme-born ******* et a broader path into consumer and enterprise crypto products.

The official corporate arm of the Dogecoin Foundation, along with merger partner Brag House Holdings Inc. (NASDAQ: $TBH), said Monday that Dogecoin will be integrated across Paxos’ enterprise-grade crypto brokerage and custody infrastructure. Paxos powers crypto services for platforms including PayPal (NASDAQ: $PYPL), Venmo, Interactive Brokers (NASDAQ: $IBKR) and Mercado Libre, putting Dogecoin closer to distribution channels that already touch large consumer audiences.

The partnership does not automatically place DOGE inside every Paxos client product. It gives enterprise platforms using Paxos infrastructure the ability to evaluate Dogecoin support through a regulated custody, liquidity and compliance layer. For House of Doge, that distinction is important: the work is less about another exchange listing and more about making Dogecoin easier for fintech platforms to offer at scale.

More From Cryptoprowl:

Ripple, The Company Behind XRP, Is Valued At $50 Billion

The official corporate arm of the Dogecoin Foundation, along with merger partner Brag House Holdings Inc. (NASDAQ: $TBH), said Monday that Dogecoin will be integrated across Paxos’ enterprise-grade crypto brokerage and custody infrastructure. Paxos powers crypto services for platforms including PayPal (NASDAQ: $PYPL), Venmo, Interactive Brokers (NASDAQ: $IBKR) and Mercado Libre, putting Dogecoin closer to distribution channels that already touch large consumer audiences.

The partnership does not automatically place DOGE inside every Paxos client product. It gives enterprise platforms using Paxos infrastructure the ability to evaluate Dogecoin support through a regulated custody, liquidity and compliance layer. For House of Doge, that distinction is important: the work is less about another exchange listing and more about making Dogecoin easier for fintech platforms to offer at scale.

More From Cryptoprowl:

Ripple, The Company Behind XRP, Is Valued At $50 Billion

2 days ago

Our ******* ysts just identified a stock with the potential to be the next Nvidia. Tell us how you invest and we'll show you why it's our #1 pick. Tap here.

Abivax SA shares suffered a spectacular collapse on Tuesday, cratering as much as 40% in Paris and New York.

The clinical-stage drugmaker dropped highly anticipated Phase 3 maintenance data for its lead ulcerative colitis pill, obefazimod. The headline numbers revealed unmatched long-term efficacy, putting the company on a direct flight path to challenge big-pharma incumbents. However, the victory was instantly derailed by the appearance of scattered cancer cases concentrated exclusively in the high-dose cohort, spooking institutional investors and prompting an immediate, high-profile ******* yst downgrade.

The results from the global 44-week ABTECT maintenance study originally looked like a best-case scenario. Evaluating patients with moderately to severely active ulcerative colitis — many of whom were completely refractory, having failed multiple advanced biologic therapies — obefazimod proved to be an absolute clinical powerhouse. Patients on either the 25 mg or 50 mg once-daily oral doses achieved clinical remission rates of 50.8% and 51.3%, respectively. This stands in contrast to a meager 10.4% baseline for the placebo group, securing a placebo-adjusted remission rate of roughly 40%.

The financial wheels fell off, however, when investors opened the safety appendix. In the higher 50 mg treatment arm, investigators recorded individual diagnoses of prostate cancer, breast cancer, and colonic dysplasia — an abnormal cell progression that often acts as a precursor to malignant tumors. The high-dose cluster also flagged four separate non-melanoma skin cancer cases.

Abivax SA shares suffered a spectacular collapse on Tuesday, cratering as much as 40% in Paris and New York.

The clinical-stage drugmaker dropped highly anticipated Phase 3 maintenance data for its lead ulcerative colitis pill, obefazimod. The headline numbers revealed unmatched long-term efficacy, putting the company on a direct flight path to challenge big-pharma incumbents. However, the victory was instantly derailed by the appearance of scattered cancer cases concentrated exclusively in the high-dose cohort, spooking institutional investors and prompting an immediate, high-profile ******* yst downgrade.

The results from the global 44-week ABTECT maintenance study originally looked like a best-case scenario. Evaluating patients with moderately to severely active ulcerative colitis — many of whom were completely refractory, having failed multiple advanced biologic therapies — obefazimod proved to be an absolute clinical powerhouse. Patients on either the 25 mg or 50 mg once-daily oral doses achieved clinical remission rates of 50.8% and 51.3%, respectively. This stands in contrast to a meager 10.4% baseline for the placebo group, securing a placebo-adjusted remission rate of roughly 40%.

The financial wheels fell off, however, when investors opened the safety appendix. In the higher 50 mg treatment arm, investigators recorded individual diagnoses of prostate cancer, breast cancer, and colonic dysplasia — an abnormal cell progression that often acts as a precursor to malignant tumors. The high-dose cluster also flagged four separate non-melanoma skin cancer cases.

2 days ago

By Stephen Nellis

SAN FRANCISCO, June 2 (Reuters) - Micron Technology's march toward a $1 trillion valuation is nothing if not dramatic: a year ago it was a little over $100 billion.

That surge, though, was not built on its famed frugality, but on a nearly too-late push from Nvidia that pulled the U.S. memory chipmaker into the center of the AI boom.

For decades, the Idaho-based company survived by building factories on a shoestring budget, adopting used equipment and avoiding cutting-edge bets. That discipline helped it endure brutal boom-bust cycles in memory chips and outlast rivals, leaving it one of three global suppliers alongside South Korea’s Samsung Electronics and SK Hynix.

But that approach of treating memory chips as a commodity clashed with Nvidia’s vision for AI.

SAN FRANCISCO, June 2 (Reuters) - Micron Technology's march toward a $1 trillion valuation is nothing if not dramatic: a year ago it was a little over $100 billion.

That surge, though, was not built on its famed frugality, but on a nearly too-late push from Nvidia that pulled the U.S. memory chipmaker into the center of the AI boom.

For decades, the Idaho-based company survived by building factories on a shoestring budget, adopting used equipment and avoiding cutting-edge bets. That discipline helped it endure brutal boom-bust cycles in memory chips and outlast rivals, leaving it one of three global suppliers alongside South Korea’s Samsung Electronics and SK Hynix.

But that approach of treating memory chips as a commodity clashed with Nvidia’s vision for AI.

2 days ago

The artificial intelligence (AI) memory chip sector is experiencing something of a renaissance at the moment. As of 3 p.m. ET on May 27, both SK Hynix and Micron Technology (NASDAQ: MU) have entered the trillion-dollar club -- boasting market caps of $1.1 trillion and $1 trillion, respectively.

This milestone reflects much more than robust earnings or an encouraging future outlook. Rather, it signals a fundamental rerating of memory's critical importance in the AI infrastructure era.

Will AI create the world's first trillionaire? Our team just released a report on the one little-known company, called an "Indispensable Monopoly" providing the critical technology Nvidia and Intel both need. Continue »

Over the last year, memory has become a critical bottleneck within AI data centers. Traditional DRAM struggles to keep pace with the latency and bandwidth needs of next-generation AI accelerators. High-bandwidth memory (HBM) layers memory dies to produce dramatically higher bandwidth.

SK Hynix and Micron have captured leading share in supplying HBM to graphics processing unit (GPU) designers like Nvidia. For now, supply chains are constrained as demand is effectively pre-sold for extended periods. These dynamics have shifted significant pricing power toward memory producers. As a result, SK Hynix and Micron are generating historically high revenue while also expanding profit margins.

This milestone reflects much more than robust earnings or an encouraging future outlook. Rather, it signals a fundamental rerating of memory's critical importance in the AI infrastructure era.

Will AI create the world's first trillionaire? Our team just released a report on the one little-known company, called an "Indispensable Monopoly" providing the critical technology Nvidia and Intel both need. Continue »

Over the last year, memory has become a critical bottleneck within AI data centers. Traditional DRAM struggles to keep pace with the latency and bandwidth needs of next-generation AI accelerators. High-bandwidth memory (HBM) layers memory dies to produce dramatically higher bandwidth.

SK Hynix and Micron have captured leading share in supplying HBM to graphics processing unit (GPU) designers like Nvidia. For now, supply chains are constrained as demand is effectively pre-sold for extended periods. These dynamics have shifted significant pricing power toward memory producers. As a result, SK Hynix and Micron are generating historically high revenue while also expanding profit margins.

3 days ago

Agilent Technologies, Inc. (NYSE:A) was among the stocks Jim Cramer was focused on, as he discussed Mad Money’s latest game plan for the week. Cramer discussed the company’s latest earnings during the episode, as he stated:

What do we make of these results from Agilent, letter A, one of the major arms dealers to the life sciences industry, among other precision enterprises? Earlier this week, the company reported a magnificent top and bottom-line beat, with management also raising their full-year forecast. Yesterday, the stock, in response, jumped 17%, although it’s still basically just flat year to date, so there might be an opportunity.

This quarter was interesting because some of Agilent’s key end markets were indeed weak: China, food, academic, government spending down. But the rest of the business was so good, it more than made up for that softness. We’re talking about strengthening drug development, drug manufacturing, cancer diagnostics, semiconductor material testing, airport security screening, and lab automation. Next week, they’re presenting data on some new products at the American Society of Mass Spectrometry meeting, and it’s going to be very important.

Photo by Anna Nekrashevich on Pexels

Agilent Technologies, Inc. (NYSE:A) provides instruments, software, and services for life sciences, diagnostics, and chemical ****** ysis, including chromatography, spectroscopy, genomics, and laboratory automation solutions.

What do we make of these results from Agilent, letter A, one of the major arms dealers to the life sciences industry, among other precision enterprises? Earlier this week, the company reported a magnificent top and bottom-line beat, with management also raising their full-year forecast. Yesterday, the stock, in response, jumped 17%, although it’s still basically just flat year to date, so there might be an opportunity.

This quarter was interesting because some of Agilent’s key end markets were indeed weak: China, food, academic, government spending down. But the rest of the business was so good, it more than made up for that softness. We’re talking about strengthening drug development, drug manufacturing, cancer diagnostics, semiconductor material testing, airport security screening, and lab automation. Next week, they’re presenting data on some new products at the American Society of Mass Spectrometry meeting, and it’s going to be very important.

Photo by Anna Nekrashevich on Pexels

Agilent Technologies, Inc. (NYSE:A) provides instruments, software, and services for life sciences, diagnostics, and chemical ****** ysis, including chromatography, spectroscopy, genomics, and laboratory automation solutions.

3 days ago

New Jersey Resources Corporation (NYSE:NJR) ranks among the top hydrogen stocks to buy now. On May 20, Argus upgraded the price target for New Jersey Resources Corporation (NYSE:NJR) to $63 from $58 while maintaining a Buy rating on the company’s shares following its fiscal second-quarter 2026 earnings, which exceeded forecasts.

New Jersey Resources Corporation (NYSE:NJR) reported net financial earnings per share of $2.20 for the quarter, rising 24% from $1.78 in the same period the previous year. The results came in far above **** yst forecasts, with the company’s Energy Services sector taking advantage of unpredictable winter market circumstances.

Overall, the Energy Services segment had the best performance, providing $37.0 million in Q2 NFE and $45.4 million year-to-date, thanks to natural gas price swings and the company’s long-option positioning approach. Clean Energy Ventures, on the other hand, recorded a $1.3 million loss in the second quarter and $39.8 million year-to-date, indicating the onset of project development and construction operations.

New Jersey Resources Corporation (NYSE:NJR) is a holding company. It provides regulated natural gas distribution, transmission, and storage services, as well as certain unregulated enterprises. It operates across five segments: natural gas distribution, clean energy ventures, energy services, storage and transportation, and home services and other services.

While we acknowledge the potential of BLDP as an investment, we believe certain AI stocks offer greater upside potential and carry less downside risk. If you're looking for an extremely undervalued AI stock that also stands to benefit significantly from Trump-era tariffs and the onshoring trend, see our free report on the best short-term AI stock.

New Jersey Resources Corporation (NYSE:NJR) reported net financial earnings per share of $2.20 for the quarter, rising 24% from $1.78 in the same period the previous year. The results came in far above **** yst forecasts, with the company’s Energy Services sector taking advantage of unpredictable winter market circumstances.

Overall, the Energy Services segment had the best performance, providing $37.0 million in Q2 NFE and $45.4 million year-to-date, thanks to natural gas price swings and the company’s long-option positioning approach. Clean Energy Ventures, on the other hand, recorded a $1.3 million loss in the second quarter and $39.8 million year-to-date, indicating the onset of project development and construction operations.

New Jersey Resources Corporation (NYSE:NJR) is a holding company. It provides regulated natural gas distribution, transmission, and storage services, as well as certain unregulated enterprises. It operates across five segments: natural gas distribution, clean energy ventures, energy services, storage and transportation, and home services and other services.

While we acknowledge the potential of BLDP as an investment, we believe certain AI stocks offer greater upside potential and carry less downside risk. If you're looking for an extremely undervalued AI stock that also stands to benefit significantly from Trump-era tariffs and the onshoring trend, see our free report on the best short-term AI stock.

3 days ago

Tech stocks ended last week with gains as the Nasdaq 100 (^NDX) crossed the 30,000 mark for the first time amid cautious optimism for an extended ceasefire agreement between the US and Iran.

The tech sector faces its next series of tests this week as a raft of labor data offers insight into how artificial intelligence is affecting the workforce, more chip and cybersecurity companies release their quarterly results, and the world’s chip giants descend on Taiwan for the annual Computex Taipei conference.

On June 1, Nvidia CEO Jensen Huang delivered his keynote address at the chip summit, where he stated that “AI is now a profit generator” and expanded upon the company’s products, particularly its Vera Rubin AI platform.

In the private markets, Anthropic (ANTH.PVT) announced last week that it had completed its Series H funding round, valuing the company at $965 billion, making the Claude Code creator more valuable than OpenAI (OPAI.PVT) and the most valuable AI startup in the world. Anthropic also released an update to its flagship Opus 4.8 model last Thursday.

Investors continue to **** s what the looming mega IPOs from Anthropic, OpenAI, and **** eX (SPAX.PVT) mean for the booming AI and tech trade.

The tech sector faces its next series of tests this week as a raft of labor data offers insight into how artificial intelligence is affecting the workforce, more chip and cybersecurity companies release their quarterly results, and the world’s chip giants descend on Taiwan for the annual Computex Taipei conference.

On June 1, Nvidia CEO Jensen Huang delivered his keynote address at the chip summit, where he stated that “AI is now a profit generator” and expanded upon the company’s products, particularly its Vera Rubin AI platform.

In the private markets, Anthropic (ANTH.PVT) announced last week that it had completed its Series H funding round, valuing the company at $965 billion, making the Claude Code creator more valuable than OpenAI (OPAI.PVT) and the most valuable AI startup in the world. Anthropic also released an update to its flagship Opus 4.8 model last Thursday.

Investors continue to **** s what the looming mega IPOs from Anthropic, OpenAI, and **** eX (SPAX.PVT) mean for the booming AI and tech trade.