OpenAI is going public as the most expensive AI company in its peer group—not by market cap, but by what investors are paying for each unit of business quality, according to our latest research. The company’s upcoming disclosures will test whether that premium is justified or just momentum.

OpenAI’s path to profitability rests on a contract with an expiration date. In April, it renegotiated its revenue-share agreement with Microsoft, capping payments at $38 billion through 2030 and saving an estimated $70 to $97 billion. Without that cap, positive free cash flow is not possible. Investors must price the listing based on an agreement whose most consequential provisions haven’t been written.

The company’s revenue is real, but the economics are broken. Q1 revenue hit $5.7 billion, yet at a negative 122% adjusted operating margin, OpenAI spent $2.22 for every dollar earned. To justify an $852 billion valuation, the company would need to generate $95 billion to $105 billion in free cash flow by 2030. Based on Q1 numbers, it is on track to lose between $10 billion and $30 billion that year instead.

Sign up for The Daily Pitch newsletter Subscribe

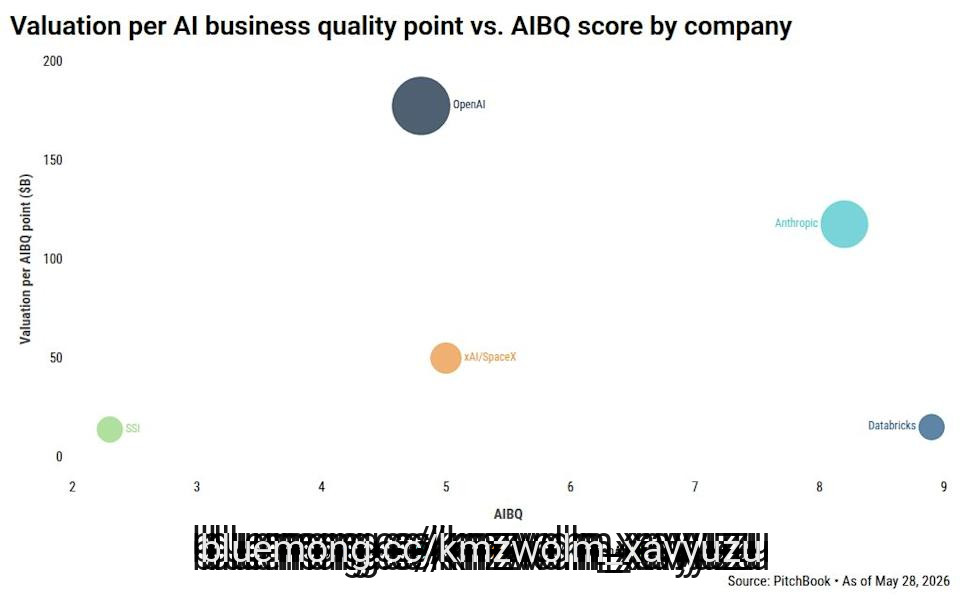

Our AI Business Quality (AIBQ) scorecard puts OpenAI last among its peers at 4.8 out of 10. At an $852 billion valuation, that works out to $177.5 billion per AIBQ point—11.8 times what investors pay for Databricks. Its main competitor, Anthropic, is pursuing a parallel listing with higher run-rate ARR (estimated $47 billion vs. $25 to $33 billion for OpenAI), a faster path to profitability, and the enterprise market share lead (40% vs. 27%).

OpenAI’s path to profitability rests on a contract with an expiration date. In April, it renegotiated its revenue-share agreement with Microsoft, capping payments at $38 billion through 2030 and saving an estimated $70 to $97 billion. Without that cap, positive free cash flow is not possible. Investors must price the listing based on an agreement whose most consequential provisions haven’t been written.

The company’s revenue is real, but the economics are broken. Q1 revenue hit $5.7 billion, yet at a negative 122% adjusted operating margin, OpenAI spent $2.22 for every dollar earned. To justify an $852 billion valuation, the company would need to generate $95 billion to $105 billion in free cash flow by 2030. Based on Q1 numbers, it is on track to lose between $10 billion and $30 billion that year instead.

Sign up for The Daily Pitch newsletter Subscribe

Our AI Business Quality (AIBQ) scorecard puts OpenAI last among its peers at 4.8 out of 10. At an $852 billion valuation, that works out to $177.5 billion per AIBQ point—11.8 times what investors pay for Databricks. Its main competitor, Anthropic, is pursuing a parallel listing with higher run-rate ARR (estimated $47 billion vs. $25 to $33 billion for OpenAI), a faster path to profitability, and the enterprise market share lead (40% vs. 27%).

1 day ago