2 hours ago

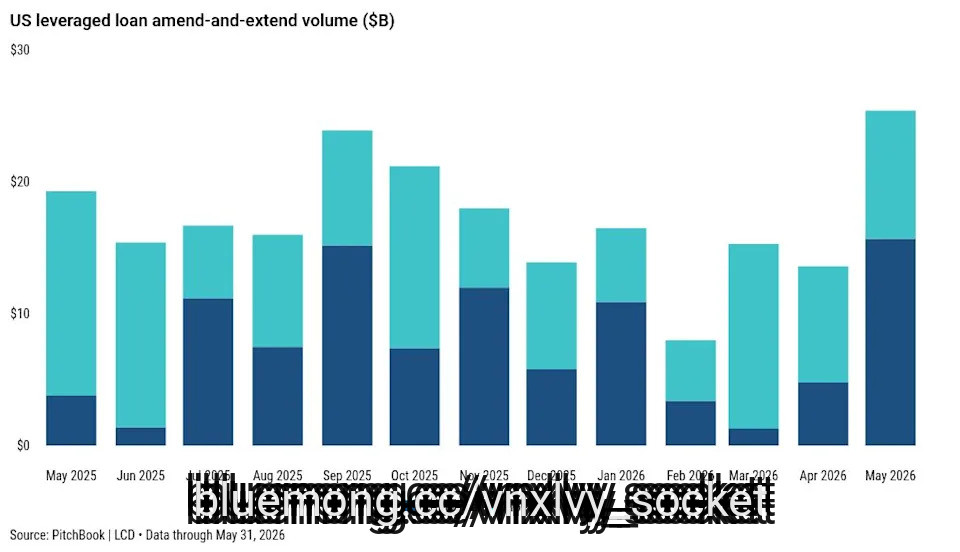

Amend-and-extend loan volume jumped to $25.4 billion in May, a high for any month since June 2024, according to LCD.

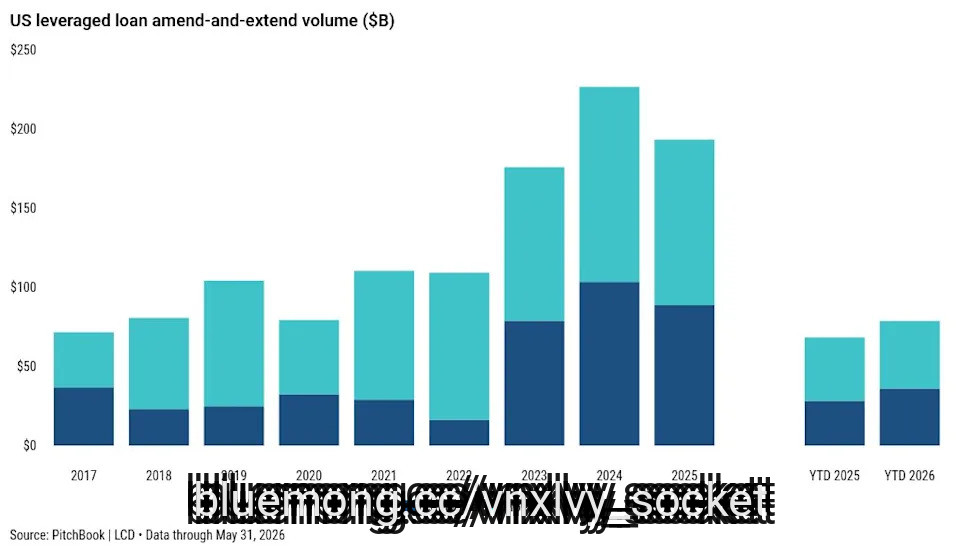

May's amend-and-extend activity came via 19 transactions, up from 18 transactions (for $13.6 billion) in April. Nearly $79 billion of volume this year is up from roughly $68 billion through the first five months of 2025.

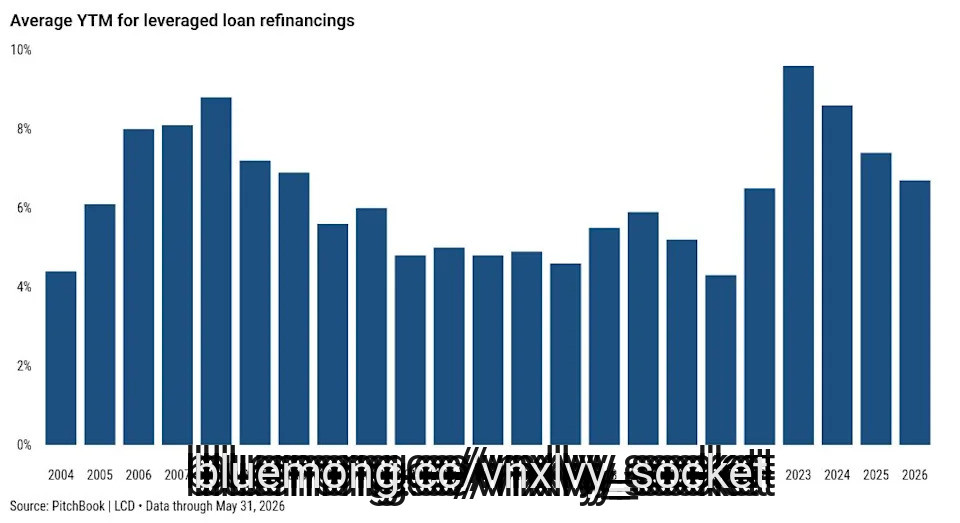

Borrowers continued to seek amendments, as opposed to refinancings, to take out credit facilities. The average yield to maturity for refinancing institutional term loans via syndication currently stands at 6.7% for 2026, which is lower than 7.4% in 2025 and the 8.6% in 2024, but still elevated from all the years spanning 2011-2022.

Year-to-date, the distribution between institutional A-and-E issuance ($36.2 billion) and pro rata issuance ($42.7 billion) has been fairly balanced. May's A-and-E activity was concentrated in institutional deals ($15.7 billion, versus $9.7 billion in pro rata volume).

Note that pro rata debt typically entails amortizing TLAs and/or revolving credit facilities and is traditionally syndicated to finance companies and banks. Institutional debt consists of term loans structured specifically for institutional investors, including CLOs.

May's amend-and-extend activity came via 19 transactions, up from 18 transactions (for $13.6 billion) in April. Nearly $79 billion of volume this year is up from roughly $68 billion through the first five months of 2025.

Borrowers continued to seek amendments, as opposed to refinancings, to take out credit facilities. The average yield to maturity for refinancing institutional term loans via syndication currently stands at 6.7% for 2026, which is lower than 7.4% in 2025 and the 8.6% in 2024, but still elevated from all the years spanning 2011-2022.

Year-to-date, the distribution between institutional A-and-E issuance ($36.2 billion) and pro rata issuance ($42.7 billion) has been fairly balanced. May's A-and-E activity was concentrated in institutional deals ($15.7 billion, versus $9.7 billion in pro rata volume).

Note that pro rata debt typically entails amortizing TLAs and/or revolving credit facilities and is traditionally syndicated to finance companies and banks. Institutional debt consists of term loans structured specifically for institutional investors, including CLOs.